[ad_1]

Right now, we current a visitor submit written by David Papell and Ruxandra Prodan, Professor and Educational Affiliate Professor of Economics on the College of Houston.

The Federal Open Market Committee (FOMC) raised the goal vary for the federal funds fee (FFR) by 25 foundation factors to between 4.5 and 4.75 % in its January/February 2023 assembly and anticipated that ongoing will increase can be acceptable. This adopted fee will increase totaling 4.25 share factors between March and December 2022 preceded by two years on the Efficient Decrease Certain (ELB).

There’s widespread settlement that the Fed fell “behind the curve” by not elevating charges when inflation rose in 2021, forcing it to play “catch-up” in 2022. “Behind the curve,” nonetheless, is meaningless with no measure of “on the curve.” Within the newest model of our paper, “Coverage Guidelines and Ahead Steerage Following the Covid-19 Recession,” we use knowledge from the Abstract of Financial Projections (SEP) from September 2020 to December 2022 to match coverage rule prescriptions with precise and FOMC projections of the FFR. This gives a exact definition of “behind the curve” because the distinction between the FFR prescribed by the coverage rule and the precise or projected FFR. We analyze 4 coverage guidelines:

The Taylor (1993) rule with an unemployment hole is as follows,

the place is the extent of the short-term federal funds rate of interest prescribed by the rule, is the inflation fee, is the two % goal degree of inflation, is the 4 % fee of unemployment within the longer run, is the present unemployment fee, and is the ½ % impartial actual rate of interest from the present SEP.

Yellen (2012) analyzed the balanced strategy rule the place the coefficient on the inflation hole is 0.5 however the coefficient on the unemployment hole is raised to 2.0.

The balanced strategy rule obtained appreciable consideration following the Nice Recession and have become the usual coverage rule utilized by the Fed.

The FOMC adopted a far-reaching Revised Assertion on Longer-Run Objectives and Financial Coverage Technique in August 2020. The framework comprises two main modifications from the unique 2012 assertion. First, coverage selections will try to mitigate shortfalls, fairly than deviations, of employment from its most degree. Second, the FOMC will implement Versatile Common Inflation Focusing on (FAIT) the place, “following durations when inflation has been operating persistently beneath 2 %, acceptable financial coverage will doubtless intention to attain inflation reasonably above 2 % for a while.”

Whereas many of the consideration following the Revised Assertion targeted on FAIT, the massive rise in inflation in 2021 and 2022 has made that half irrelevant. The balanced strategy (shortfalls) rule was launched within the February 2021 Financial Coverage Report (MPR). The rule mitigates employment shortfalls as a substitute of deviations by having the FFR solely reply to unemployment if it exceeds longer-run unemployment,

If unemployment exceeds longer-run unemployment, the FFR prescriptions are the identical as with the balanced strategy rule. If unemployment is beneath longer-run unemployment, the FOMC won’t increase the FFR solely due to low unemployment. We additionally analyze a Taylor (shortfalls) rule,

These guidelines are non-inertial as a result of the FFR totally adjusts every time the goal FFR modifications. This isn’t in accord with FOMC observe to easy fee will increase when inflation rises. Throughout 2021 and 2022, the non-inertial guidelines prescribe unrealistically massive will increase of the FFR.

We specify inertial variations of the foundations primarily based on Clarida, Gali, and Gertler (1999),

the place is the diploma of inertia and is the goal degree of the federal funds fee prescribed by Equation (3). We set as in Bernanke, Kiley, and Roberts (2019). equals the speed prescribed by the rule whether it is optimistic and 0 if the prescribed fee is unfavourable.

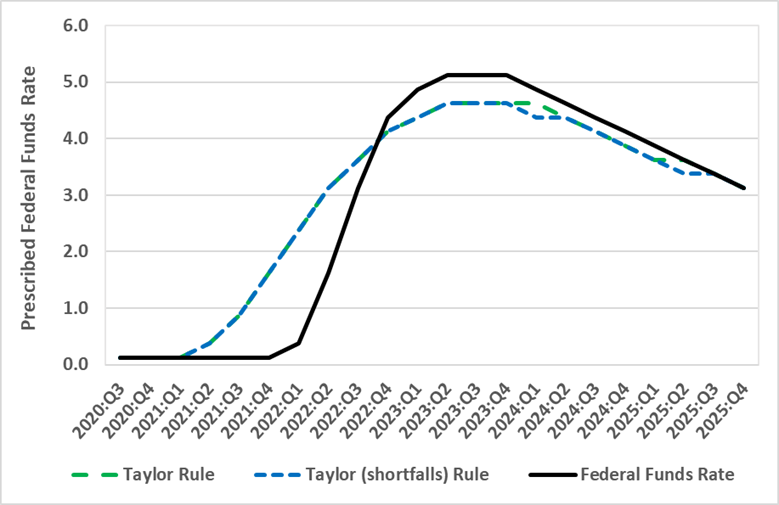

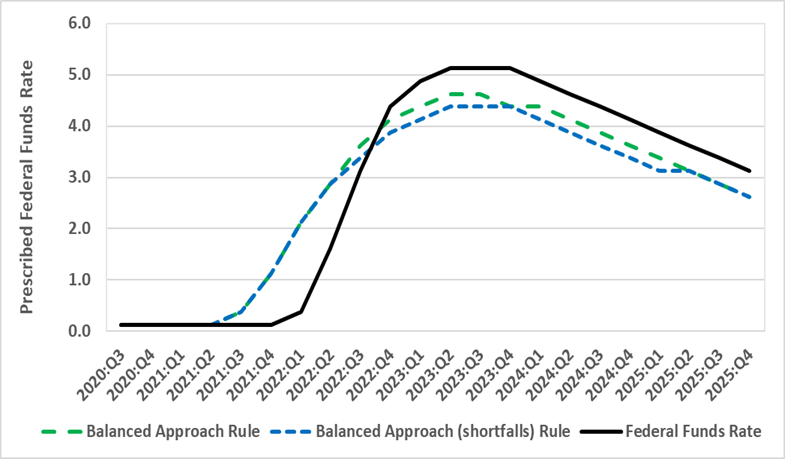

The determine depicts the midpoint for the goal vary of the FFR for September 2020 to December 2022 and the projected FFR for March 2023 to December 2025 from the December 2022 SEP. Following the exit from the ELB to 0.375 in March 2022, the FFR rose to 4.625 in February 2023 and is projected to rise to five.125 in June 2023 earlier than falling in 2024 and 2025.

Determine 1, Panel A: Inertial Coverage Guidelines and the Federal Funds Charge – Taylor Rule

Coverage rule prescriptions are reported in Panel A for the Taylor guidelines and Panel B for the balanced strategy guidelines. Between September 2020 and December 2022, we use real-time inflation and unemployment knowledge that was out there on the time of the FOMC conferences. Between March 2023 and December 2025, we use inflation, unemployment, and actual FFR within the longer-run projections from the December 2022 SEP.

Determine 1, Panel B: Inertial Coverage Guidelines and the Federal Funds Charge – Balanced Strategy Guidelines.

The FFR fell “behind the curve” when the prescribed FFR elevated above the ELB in June 2021 for the Taylor guidelines and September 2021 for the balanced strategy guidelines. The hole peaked at 200 foundation factors for the Taylor guidelines and 175 foundation factors for the balanced strategy guidelines on the liftoff from the ELB in March 2022. Because the FOMC aggressively raised the FFR, the hole narrowed to 25 foundation factors above the FFR in September 2022 for the balanced strategy (shortfalls) rule and 50 foundation factors above the FFR for the opposite three guidelines.

We spotlight two factors illustrated in Determine 1. First, as described in additional element within the paper, the FOMC might have achieved the identical improve within the FFR by September 2022 with out resorting to 75 foundation level fee will increase by following any of the coverage guidelines. Second, the balanced strategy guidelines prescriptions are nearer to the trail of the FFR than the Taylor guidelines prescriptions.

The relation between the precise and prescribed FFR’s reversed in December 2022, because the FFR is 50 foundation factors above the prescribed FFR for the balanced strategy (shortfalls) rule and 25 foundation factors above the FFR for the opposite three guidelines. For 2023 – 2025, the determine exhibits the FFR projected by the December 2022 SEP and the FFR prescribed by the coverage guidelines utilizing knowledge projected from the December 2022 SEP. The gaps widen by December 2023 after which slender because the FFR projections lower.

The relation between the Taylor rule and balanced strategy rule prescriptions additionally reverses with the December 2025 SEP, because the gaps between the FFR projections and the coverage rule prescriptions are smaller for the Taylor guidelines than for the balanced strategy guidelines. Beginning in March 2024, the gaps for the Taylor rule slender to 25 foundation factors and, between June and December of 2025, the Taylor rule prescriptions are equal to the FFR projections.

This submit written by David Papell and Ruxandra Prodan.

[ad_2]