[ad_1]

What’s the present state of the macroeconomy?

First, and most vital, and maintain to this: the inflation expectations implicit in bond costs inform us that the marginal energetic dealer betting on such issues within the bond market expects Client Worth Index (CPI) inflation between 5 and ten years from now to be 2.3% per 12 months. That’s smack in the midst of the two.0% to 2.5% vary on the CPI that signifies that the Federal Reserve is nailing its 2.0% per 12 months Private Consumption Expenditures (PCE) inflation goal. Thus the bond market expects that the Federal Reserve has accomplished or will do no matter it takes to get inflation to its goal within the five- to ten-year medium run:

That is most vital as a result of bond merchants are essentially the most simply scared and flighty of individuals so far as expectations of inflation are involved. First, their loss perform is very asymmetrical: inflation damages their portfolios mightily. Second, they speak to one another an excessive amount of, and thus give one another far more confidence within the outcomes of their groupthink. If bond merchants don’t anticipate the Fed to overlook its inflation goal within the medium run, it’s extremely unlikely that there’s any group—staff, managers, fairness buyers, commodity suppliers, and so forth—that thinks that the Fed goes to overlook its inflation goal on the upside, and is therefore planning that relaxation on that end result.

That has highly effective implications for the usual Phillips Curve, utilizing π for inflation:

(pi = E(pi) + beta(u^* – u) + epsilon)

precise inflation equals anticipated inflation, plus the sensitivity of present inflation to demand instances the distinction between the pure and the precise charge of unemployment, plus all of the shocks to the financial system. Stagflation happens when a excessive stage of inflation within the latest previous feeds again and raises expectations of inflation within the current. That may occur sometime. It’s not occurring now. The inflation that’s occurring now’s a consequence of (1) there nonetheless being post-plague reopening bottleneck shocks and Assault on Ukraine- and other-related provide shocks, plus (2) an financial system that’s working sizzling, within the sense that each staff and managers assume they’ve uncommon pricing energy to boost what they cost, and are utilizing it. What’s the division between (1) and (2). We do not know. All now we have are ill-founded guesses.

With a view to management (2), the Federal Reserve has raised its policy-control charge, the three-month Treasury Invoice charge, from zero firstly of 2022 to, presently, 4.5% per 12 months, and promised to take care of it there till they’re assured that inflation is quickly shifting again to the two% per 12 months PCE goal. This enhance has been efficient: the ten-year Treasury Bond charge that’s the finest single quantity at summarizing how curiosity prices are boosting or retarding spending has risen from 1.5% per 12 months to 4.0% per 12 months—a gearing of two/3, which is considerably bigger than the usual gearing of 1/3 which we sometimes see (or used to see: issues may need modified) when lengthy bond charges react to Federal Reserve coverage strikes:

There are those that say that, truly, the Federal Reserve has not tightened in any respect: that, sure, nominal curiosity prices are greater, however as a result of debt principal is being eaten away by inflation actual curiosity prices haven’t been elevated. They’re fallacious. The market doesn’t anticipate inflation within the medium-run. Furthermore, the rise within the rate of interest on inflation-indexed bonds has been the identical 2.5%-points per 12 months—the identical 250 foundation factors—as the rise within the rate of interest on the nominal ten-year bond:

Nominal rates of interest have elevated. Related inflation expectations haven’t. Therefore actual borrowing prices have elevated. These will increase will cool off demand for funding items, client durables, housing and non-residential buildings, and, by the trade charge channel, for U.S. exports and for home manufacturing of import-competing manufactures. That cooling-off of demand will, the Federal Reserve hopes, take away the constructive contribution to inflation made by the β(u* – u) time period within the Phillips Curve, and because the reopening and provide shocks die off, depart inflation equal to anticipated inflation and therefore, because the market expects the Federal Reserve to hit its inflation goal, at 2% per 12 months.

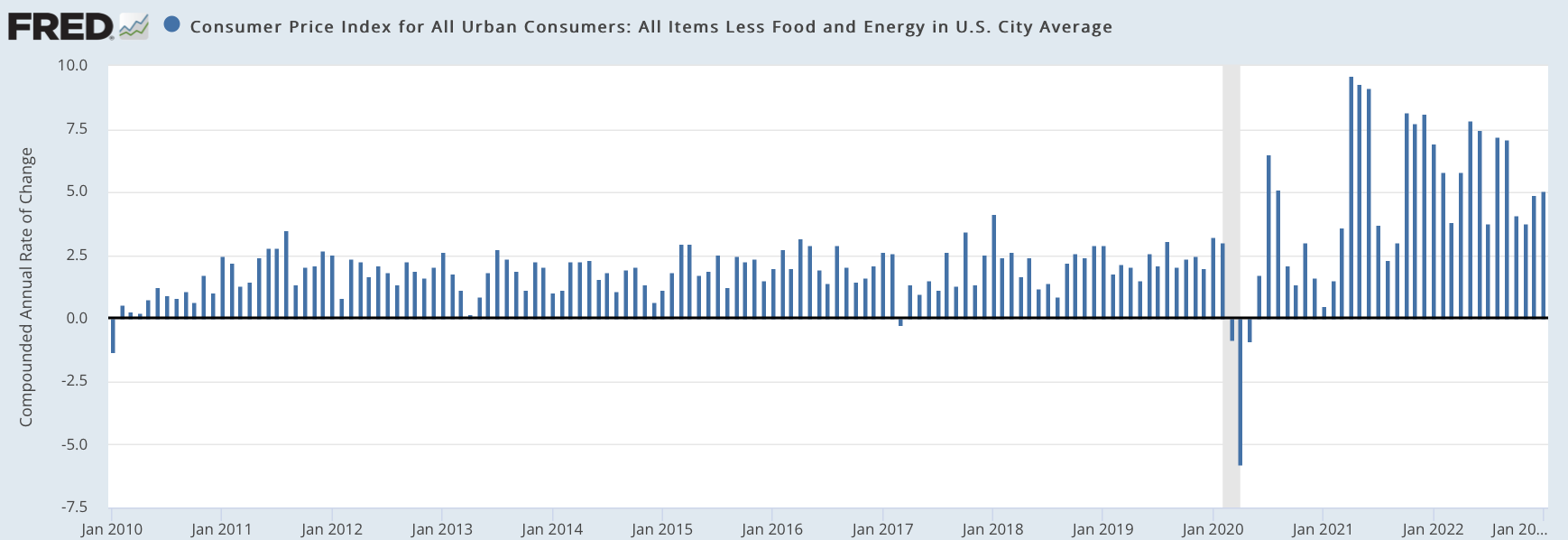

However the month-to-month core inflation—i.e., inflation eradicating unstable meals and power costs—numbers inform us that this isn’t occurring but. We now not see the 7% to 10% annualized inflation months that we noticed throughout the reopening, as we left the inevitable rubber on the highway as we tried to rejoin the freeway site visitors at velocity. It has been 5 months since we noticed a 7& annualized core-CPI month because the Assault on Ukraine adversarial provide shock labored its manner by the world financial system. However I might have anticipated annualized core inflation numbers now to begin with a “4” reasonably than a “5”, and I might have been trying ahead to months with annualized core inflation numbers beginning with a “3”. That has not occurred this winter. Thus my visualization of the Cosmic All has been awry:

My view: there may be an 80% likelihood that over spring and summer season we are going to see these “4” and “3” main digits within the annualized month-to-month reported inflation charges. However we might not. The world is a stunning place.

How a lot of a contribution is a good labor market (and product market) by which staff (and managers) assume they’ve energy to boost what they cost making to our inflation? We have no idea. Now we have no dependable and stable measures of the state of the labor market (or of the product market) because it pertains to inflation. We’re at see.

I’ve been, tentatively, trusting the stop charge:

The stop charge tells us concerning the fraction of people that assume that their outdoors prospects within the labor market are ok that they can provide in to the temptation to inform the boss to take this job and shove it. In 2019 the U.S. financial system ran with a stop charge of two.4% per 30 days (sure: per 30 days) with out anyone whining about inflation pressures within the labor market. The present stop charge is 2.6% per 30 days, down from the post-plague reopening excessive of three% per 30 days.

There are, as Milton Friedman famously mentioned, lengthy and variable lags in all of those processes. My view is that the final 100 foundation factors—the final share level per 12 months—of enhance within the lengthy bond charge from 3% per 12 months to 4% per 12 months has not but impacted the financial system in any respect, and therefore there may be downward strain on demand and thus on the willingness of employers to develop and thus on the stop charge coming. Will what the Fed has already accomplished by way of this final enhance in rates of interest handle, when it hits and has its results on spending, push the stop charge down right into a area by which there’ll now not be inflationary pressures coming from the financial system “working sizzling”?

I say in all probability.

And Paul Krugman has a view:

Paul Krugman: Wonking out: Peering by the fog of inflation: ‘In early 2021, some economists warned that expansionary fiscal coverage and free financial coverage could be extremely inflationary. As inflation started to rise, a few of us argued that it was primarily “transitory,” a results of pandemic distortions that may fade away. However inflation went far greater for longer than we anticipated, and at the least a few of Group Transitory issued mea culpas, whereas a few of those that had predicted inflation doubled down on their pessimism, with warnings of a few years of stagflation to return. Then the inflation numbers started trying significantly better, and excessive pessimism started to look foolish. However the story wasn’t over; in latest months the inflation image has begun to look considerably worse once more, and there was a palpable push by excessive inflation pessimists to insist that they had been proper all alongside…. Perhaps the essential level is simply how murky the scenario is. The reality is that we don’t have a really clear image of what’s occurring to inflation proper now…. The Fed is creeping its manner ahead by a dense information fog, and this means to me that it ought to keep away from drastic strikes in both route…. Financial observers might wish to take a deep breath and funky among the rhetoric. The reality on inflation has gotten more durable to discern, and that fog isn’t one thing a conflict of egos goes to clear away…

“Energy and weirdness” is an excellent phrase…

To the extent which you can anchor them to actuality, both by forcing them to have a look at and prioritize info, or do a search that they then belief, you should use them for good:

Ethan Mollick: Energy and Weirdness: Tips on how to Use Bing AI: ‘Bing will produce outcomes fairly just like ChatGPT till you persuade it to look one thing up. When it does, one thing magical appears to occur. Right here’s an instance: write a paragraph about consuming a meal produces fairly boring ChatGPT-like prose. It’s by no means unhealthy, however it’s bland…. However now lets ask Bing to make use of the web: search for the writing kinds of Ruth Reichl and Anthony Bourdain. Use what you will have realized to enhance the paragraph. A number of fascinating issues occur because of this. First, you’ll be able to see Bing performs an online search (the check-mark on the prime). Subsequent, you will note it makes use of this search to offer annotations and sources, that are clickable. They don’t all the time go to the precisely appropriate supply, however they normally do. Lastly, you’ll discover the writing has modified rather a lot. The reply is extra subtle and the textual content is definitely fascinating to learn…

In any other case…

Robert Bates discusses the legacy of Doug North:

-

Francis Wilkinson: Fox Information Is Trapped by Its Personal Zealotry: ‘Worry of dropping viewers to extra fervent purveyors of the Trump gospel finally ensnared the community in a $1.6 billion defamation swimsuit…

-

Kaushik Basu: How Singapore Impresses: ‘There are various causes for Singapore’s fast progress over the previous six many years, however its authoritarian regime isn’t essentially one in every of them. As an alternative, the city-state’s financial miracle has extra to do with its distinctive model of multiculturalism and enviable social cohesion…

-

Jamelle Bouie: ‘Only a hilarious quantity of corruption swirling across the supreme court docket: Heidi Przybyla: “Darkish cash and particular offers: How Leonard Leo and his mates benefited from his judicial activism: The Federalist Society co-chairman’s way of life took a lavish flip after he grew to become Donald Trump’s adviser on judicial nominations…

-

David Rovella: China Leans Into Battle for Tech Supremacy: ‘Chinese language web moguls are being changed by chip researchers and engineers on key lawmaking and advisory our bodies, a possible signal of Beijing’s lingering mistrust for personal enterprise and sharpening deal with the tech race…

-

Ilari Mäkelä: On People Podcast ~ Science and Philosophy of Our Shared Humanity…

Josh Marshall: Dispatch No. 55: Let’s Have a look at the Deep Archeology of Fox Information: ‘The proof rising from the Dominion lawsuit towards Fox Information has the standard of liberal fever goals. What’s the worst you’ll be able to presumably think about about Fox? What’s essentially the most cartoonish caricature, the worst it may presumably be? Properly, in these emails and texts you principally have that. Solely it’s actual. It’s not anybody believing the worst and giving no advantage of the doubt. That is what Fox is…. Over the course of the Sixties and Seventies they set about attempting to construct a collection of counter-institutions…. Brookings was mainstream, stodgy, quasi-academic. Heritage was completely ideological and partisan. In apply it was normally little greater than a propaganda mill for the proper. This sample was duplicated numerous instances…. What we see right now in Fox Information is a lot of the story: a purported information group that knowingly and repeatedly experiences lies to its viewers…. What has all the time been the inform about Fox Information is the tagline and motto: honest and balanced. The operation’s very branding is an aggressive little bit of trolling. An unabashedly partisan and ideological operation promoting itself beneath the heading of “honest and balanced.” It’s much less a lie than a figuring out taunt…. [Tucker] Carlson… launched The Each day Caller…. However what shortly grew to become clear is that there was little viewers, market or demand for that sort of conservative publication [that did not tell its audience the lies they wanted to hear]. To no matter extent Carlson had ever actually been dedicated to creating that sort of publishing operation, he shortly misplaced endurance with it and shifted gears to the publication we’ve been acquainted with for the final dozen years: a barely much less transgressive and racist model of Breitbart. There merely wasn’t any future or cash in that different sort of operation…

Reid Robinson: Tips on how to write an efficient GPT-3 immediate: ‘1. Provide context; 2. Embody useful data upfront; 3. Give examples; 4. Inform it the size of the response you need; 5. Outline the anticipated codecs: 6. Use a few of these helpful expressions:”Let’s assume step-by-step”, “Pondering backwards”, “Within the model of [famous person]”, “As a [insert profession/role]”…

[ad_2]