[ad_1]

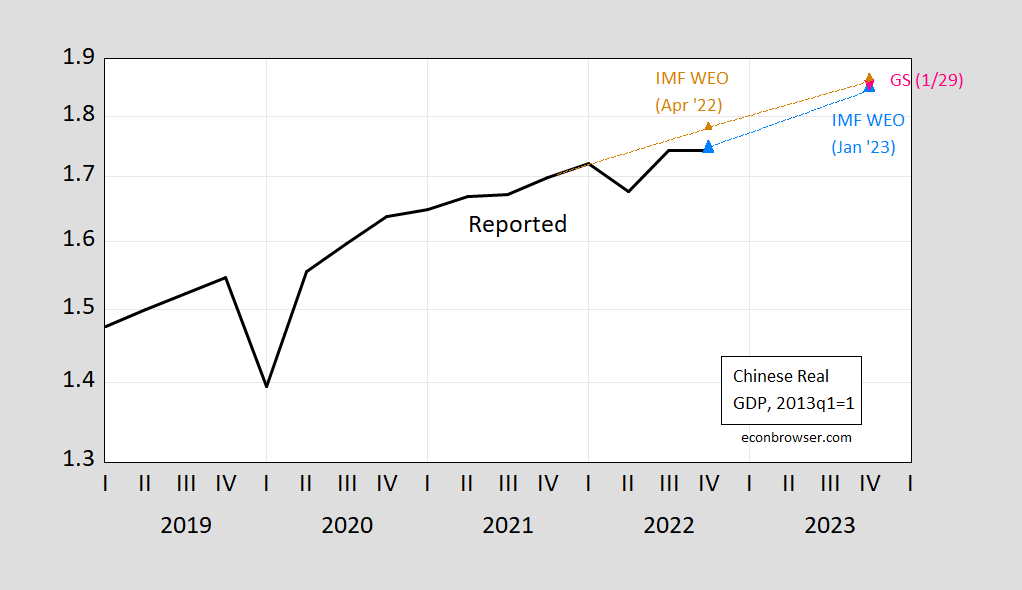

Chinese language GDP for this fall was launched a pair weeks in the past, present a resumption of progress. The IMF has upped its progress forecast (WEO), relative to October’s, by almost a share level (y/y). Nonetheless, the extent of GDP will match roughly what was anticipated again in April’s report.

Determine 1: China actual GDP index, 2013q1=1 (daring black), IMF WEO January 2023 replace projection (sky blue triangle), IMF WEO April 2022 projection (tan triangle), and Goldman Sachs 1/29 forecast (pink triangle). Actual GDP index calculated by cumulating progress charges on 2013Q1 degree = 1. Supply: Investing.com, IMF WEO (January 2023, April 2022), Goldman Sachs (1/29/2023), and writer’s calculations.

The improve to progress charges in 2023 have been due largely to the lifting of Covid restrictions. This appears to be in settlement with most forecasts I see for the Chinese language economic system, some stressing the truth that most individuals may have been contaminated and may have some immunity then encouraging the resumption of consumption. Mobility indicators via mid January help this view. Different observers (e.g., Paulson Institute) say the restoration will probably be very quick in Q1, after which a lot slower thereafter (a “sq. root”), given patterns following earlier reopenings.

[ad_2]